In point of fact, equities do not die, and the world does not end.

– Nick Murray

In last month’s article, we celebrated our incredible good fortune of being an American. This month, we celebrate yet another wonderful anniversary, this time related to the media’s sensationalism.

The Death of Equities

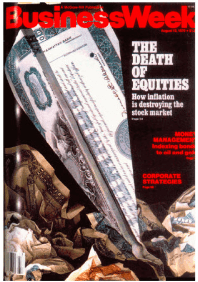

On August 13th, the world will celebrate the 40th anniversary of the publication of possibly the most ill-advised magazine cover in the history of journalism:

This cover, published by Businessweek on August 13, 1979, proclaimed that equity investing was dead and buried in the United States. Were they wrong?

- That date was the eve of one of the greatest bull markets in stocks the world has ever seen, from 1982 to 2000.

- On that date in history, the S&P 500 closed at a price of $107.42, and it now stands just a touch below 3,000.

- The dividend on the S&P 500 back then was $6, and today it is roughly $56.

- Stock prices are up approximately 30-fold, while inflation is up only around 3.5 times since then.

So much for basing your investment outlook on the predictions of financial journalists!

The Logic Of A Pessimist

This magazine cover has been a favorite of ours for a long time because it so eloquently makes the point that financial journalism and pop culture are almost always built on negativity, feeding the American investor’s fascination with Armageddon theories. For some unknown reason, pessimism is a fashionable way of thinking; human nature views the pessimist as smart and “in the know,” while the optimist is naïve and uninformed.

This cover also provides us with a wonderful example of the logic that the pessimist almost always uses to support their dire predictions of global despair. Great investors see the flaws in this logic a mile away.History has made it clear that equities do not actually die, and the world does not end. When this article was written, the U.S. stock market had survived over a century of inflation and deflation, recession and recovery, and everything in between, and it still produced a long-term return of just about 10 percent per year. The pessimist always defaults to the same devilish four words: This time is different. This time is never different; it just looks different, like it did 40 years ago.

Typically, the pessimist anticipates some worrying trend, such as the increase in inflation, to bring forth tragedy. This is another fallacy, which I call “The Extrapolation Fantasy.” These theories of doom are almost always based on the extrapolation of some undesirable trend all the way to the horizon and over the edge.

For example, one of the current Armageddon theories is that the U.S. government is piling up debt way too quickly, the rest of the world will soon stop lending us money, and the mighty dollar will lose its status as the world’s reserve currency. It is reasonable to assume that, if we keep accumulating debt at this rate, we will at some point go off the edge. Of course, the key word in that sentence is “if.”

Nobody can really argue with the statement – we don’t know the future – but the larger likelihood is that a rational democracy, faced with a crisis like that, will take action to slow down our debt. It is highly unlikely that we’ll avoid steering our ship off the edge of the world.

The Most Hated Bull Market Ever

We here at Concentus have a firm belief that investor sentiment is the most important determinant of the long-term trends in stock prices. Back in 1999, investors were so passionately in love with equities that most believed that they were entitled to a 25 percent annual return forever, and that the only risk in the stock market was the potential that your neighbor was making more money than you were. Predictably, a horrible 10-year bear market ensued. In the spring of 2009, the prevailing opinion of American investors was that the global economy was headed off of a cliff, and sentiment could only be described as “sheer terror.” Stock prices have quadrupled since then.

We have also made the case that the current trend in stock prices represents “The Most Hated Bull Market of All Time.” Amazingly, despite the fact that the last 10 years have seen one of the greatest bull markets of all time, equities continue to be feared, scorned, and shunned on an epic scale. The scars on our collective investor psyche left by 2008 still run very deep, and most investors are still waiting for the other shoe to drop.

For the latest evidence of this, we need look no further than the period between April 30th and June 20th of this year. After an all-time-high in late April, the S&P 500 got spooked by the tariff war between the U.S. and China and declined by roughly seven percent through June 3rd. Thirteen days later, on June 20th, the market was again making new highs. In the history of the S&P 500, this six-week period was an unremarkable blip on the radar: A pullback of 7 percent or so, which is quickly recovered, is an extremely common experience.

What was remarkable about this time period is how global investors responded to this momentary minor turbulence. According to Bernstein research, equity fund outflows compared to bond fund inflows were 3 standard deviations from their historic norms – in fact, they were even greater than during the 2008-2009 period. In other words, investors were dumping their stock funds and buying low yielding bond funds with even greater ferocity than back in the fall of 2008! At the same time, Merrill Lynch’s survey of 179 global money managers found allocations to equities at their lowest levels in the history of their reporting, and the month-to-month jump in cash allocations was the highest since the panic of 2011.

$13 Trillion To Lose

Market Watch recently reported that global investors now hold $13 trillion in bonds, which are trading at negative yields. In other words, $13 trillion of global capital has been allocated into fixed income securities, which are guaranteed to mature for less money than they are actually worth today, even when factoring in future interest payments!

Most of the bonds that are trading at negative yields are government bonds, largely in Europe. The investors who own these bonds are apparently so petrified about the state of affairs in the global economy that they are willing to store their capital in an investment that is guaranteed to lose money. I can honestly say that I have never seen anything quite like this in my career. It is easily the most irrational display of mass investor terror I have ever seen.

In the words of famed investor John Templeton:

Bull markets are born on pessimism, grown on skepticism, mature on optimism, and die on euphoria. The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.

Having a Plan

The media incites unnecessary panic. A Great Investor is optimistic and ignores sensationalism. It can be difficult, but our team can help you manage the emotional side of investing for the best outcome.