“Do you know the only thing that gives me pleasure? It’s to see my dividends coming in.”

– John D. Rockefeller

In last month’s article, focused on “Taking advantage of Time” as one of the great qualities to adopt for anyone who wants to become a great investor. This month we focus on slightly different quality, but another thing great investors can take advantage of…Great Investors Love Dividends.

Appreciating Dividends

If you speak with an “old dinosaur” in the investment business – someone who has been investing as a profession for many decades – you may hear an interesting insight. Investors used to invest in company shares primarily because they wanted to capture their cash dividend, and not necessarily for capital appreciation. Investors in the “old days” loved the consistent tangible return of a cash dividend. While it was always nice to buy a stock which appreciated in price, what they really wanted was the cash dividend.

In the days before the Bull Market in technology stocks in the late 1990’s, investors often invested in stocks for an income stream they felt was more reliable and consistent than what they could achieve with bonds. After all, because cash dividends represent a share of the earnings of the underlying company, a growing economy means a reliable and growing stream of income, as opposed to the “fixed” income streams offered by bonds.

Many also found it “safer” to invest in dividend stocks than in bonds, despite the inherent volatility of stock prices. A generation of investors learned well in the Great Depression that bankruptcy can entirely wipe out the claims of a lender (bondholder), while stockholders at least were owners of a business and its remaining assets. Interestingly, many equity dividend investors bought stocks in spite of the inherent volatility of stocks, and were somewhat indifferent to the possibility of upside volatility and price appreciation. While the appreciation potential was nice, they wanted that tangible check every month.

The Tech Bubble of the late 1990’s changed many things about investor psychology, but one important shift was in respect to investor attitudes about dividends. As investors became euphoric about the “high” they experienced from buying shares of technology companies, and watching their share prices race upwards in a wave of speculative energy, dividends became the forgotten vestige of investment returns. Dividends were part of the boring “Old Economy”, while capital appreciation was the reward of the New Economy investor. It seems that this attitude has persisted, and outlived the “Technology Bubble” which brought it about. Investors today continue to appear more focused on the return which comes from price appreciation, than that which arises from sharing in the cash flow of the companies they own.

Growing Cash Flow

The great investors never take anything for granted, and are thrilled to participate in the cash flows and profits of the companies they own, as a tangible reminder of their return on investment. Great investors love dividends, primarily because they tend to grow along with the profitability of the underlying companies which pay them. Dividends represent a share of a company’s profits, which is not static like the interest payment on a bond. Corporate cash flows tend to grow over time, leading to higher dividends, a trick which is difficult to pull off with a bond fund. Historically, the dividend return on the companies in the S&P 500 has grown at a rate of just about 5% per year over the last century – in fact, the dividend payment on this popular list of stocks is 65 times higher than it was at the end of World War II.

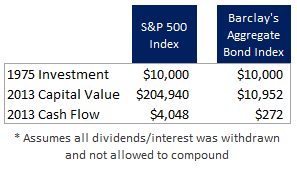

It may not be surprising to know that equity investors have achieved higher capital returns historically than bond investors have. In fact, an investor who placed $10,000 into the S&P 500 back in 1975 had a capital value of $204,940 by 2013, provided they immediately withdrew all dividend income and didn’t allow it to compound. The same $10,000 grew to $10,952 by 2013 for an investor in the Barclays Aggregate Bond index, with no compounding of income.

However, the truly astounding fact is the change in the income stream from dividends over time. A $10,000 investment in the S&P 500 in 1975 resulted in a dividend yield of $4,048 per year in dividend income by the year 2013. Yes, you read that right…ignoring the capital appreciation, an investor who placed $10,000 into the S&P 500 back in 1975 is now enjoying an annual cash flow which represents more than a 40% yield on her original investment. For comparison, the investor who placed $10,000 into the Barclay’s aggregate Bond Index back in 1975 earned interest income of $272 per year by the year 2013.

This dividend growth has occurred over all kinds of market and economic environments, and generally has been more consistent and stable than stock prices. As everyone knows, between October of 2007 and March of 2009 the S&P 500 declined by roughly 57% in price terms. In the aftermath of that crisis, the dividend payments by S&P 500 companies declined also, but not nearly as dramatically. S&P 500 dividends were a total of $32.92 at end of 2008, and fell to a low of $25.28 by the end of 2010, for a decline of roughly 23%. While this reduction was painful, it was not nearly as severe as the decline in stock prices. Dividends have now recovered to $46.38 in 2017.

100 Minus Your Age?

Popular culture and the financial media have taught investors to fear the stock market for a variety of reasons. In particular, conventional wisdom holds that it is best to reduce your ownership of company shares as you grow older. A common rule of thumb in conventional circles is that an investor should subtract her current age from 100, and the resulting number represents the portfolio percentage which should be dedicated to equities. Using this rule, the investor will gradually reduce their equity exposure over time, slowly increasing their exposure to bonds.

This rule, and the underlying logic, reflects the attitude in popular culture that older investors cannot bear the volatility inherent in owning equities, but it also reflects the common wisdom that retired investors should invest for income. The idea is that, as we grow older and perhaps retire, we need to rely on our investments to produce an income stream we can live on, and that bonds are best suited to provide such an income stream. The Great Investors rarely follow “Common Wisdom”, and usually question the answers provided by popular culture.

Life expectancy data tells us that the majority of Americans will live through a period of 30 years in retirement, and economic history tells us that inflation over time has run at an average of 3% per year. So let’s take a look at what happens to an investor’s portfolio and income over a 30 year retirement period at 3% inflation.

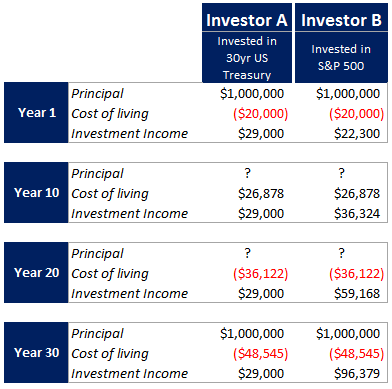

Let’s consider two investors, who are both retiring in 2017 with $1 million to invest. Both plan to spend $20,000 per year from their portfolio (in today’s dollars) and expect inflation to average 3% over the remainder of their lives.

Investor A wants to keep their portfolio “safe and conservative”, so they invest $1 million in long term 30 year Treasury bonds. At today’s yield of 2.9%, they know that they will collect $29,000 per year, which is much more than their expected spending rate of $20,000 per year. They know they will sleep well, knowing that their bonds will mature in 30 years, and return their exact $1,000,000 in principal value.

Investor B is willing to live with uncertainty, so they invest $1 million in the S&P 500. At today’s dividend yield of 2.23%, they know that they will collect $22,300 per year, which is a little less than their neighbor is receiving, but still enough to fund their anticipated expenses. They also feel confident that their dividend income stream will grow at a rate similar to the historical average of 5%. They have no idea what will happen to the principal value of the portfolio over 30 years, and have no guarantee of the return of their principal. However, since there has never been a 30 year period over which the S&P 500 has produced a negative return, they feel safe in assuming that their portfolio will at least retain its value of $1,000,000 over 30 years.

Assuming their portfolio doesn’t appreciate a single dime over 30 years, but their dividend stream increases by 5% per year as expected, the following is a comparison of our 2 investors’ results:

As this chart shows, the impact of inflation over time can be significant. At just a 3% rate of inflation, the cost of living rose by more than double over 30 years, from $20,000 per year to $48,544 per year. Investor B was able to survive the increases in cost of living, because their dividends were also rising over time, such that they always maintained a comfortable margin of annual income which exceeded their inflated cost of living. By the 30th year, they were financing the cost of living easily through their dividend return, with roughly $48,000 in extra cash flow left over. Investor A was not so lucky. Their cost of living outstripped thier fixed income stream after a little more than 10 years. After that point, their fixed income stream was not sufficient to cover living costs, so they either had to find another source of income, or go back to work! By the 30th year, their cost of living was roughly $19,000 per year higher than their fixed income stream.

Most investors think of bonds as “conservative” investments. However, in the quest to “conserve” purchasing power over time, it appears that a growing income stream is required. Although there is of course no guarantee that equity dividends will grow over time, historically dividends have provided an excellent tool for maintaining a growing income stream. The great investors look beyond slogans like “100 minus your age”.

Having a Plan

The very best investors have a disciplined approach to making portfolio decisions, and always stick to their plan, no matter what the rest of the world is doing. They always gear their investment program around the achievement of their most important life goals, and they use every tool at their disposal to do so. They understand the power of dividends as a tangible proof of their investment return over time.

No predictions, and no crystal balls. Just patience and discipline, and a share of the profits and earnings of the companies they own!

Leave A Comment