“A staggering fraud… A bank that is too big to manage”

– Senator Elizabeth Warren, referencing the recent Wells Fargo Bank fraud case

If you have picked up a newspaper or turned on the business news this week, you probably have seen images of the pained face of John Stumpf, the beleaguered CEO of Wells Fargo Bank. Unfortunately for Mr. Stumpf, he has spent his week attempting to explain to Congress why a massive fraud was committed on the bank’s customers under his watch.

Over the last few years, thousands of Wells Fargo employees have been opening millions of unauthorized bank and credit card accounts, in order to boost their sales figures and earn bigger bonuses. In the process, they subjected millions of customers to unwarranted bank fees and interest payments on accounts they never asked for. The result: over 5,300 Wells employees who engaged in this fraud have been fired, Stumpf stands to lose his job, and Wells is being forced to pay the largest penalty fine in history, reported as $185 million.

This scandal has inflicted an enormous black eye on Wells Fargo, and on the financial services industry, an industry that hardly needs any more such black eyes. The American public has come to distrust “Wall Street” and the large banks in this country, thanks to scandal after scandal that seem to never end.

Wells Fargo employs a great number of trustworthy, very high quality people – I should know because I used to work there! Unfortunately, in such a giant institution, it is difficult to police the possible bad behavior of ALL employees, and obviously oversight can become unmanageable, as it did in this case.

In the end, consumers may be left wondering if you can trust anyone in this industry.

Sales Contests

In a perfect world, financial institutions should make it their first priority to constantly look out for their clients’ and customers’ best interests. However, as this scandal exposed, that priority can sometimes directly conflict with the goal of producing more sales revenue.

The problem is very often when bankers or advisors are compensated based upon the sales of products and services, their job may become more about selling more product than it is about taking care of their client and acting as their fiduciary. Clearly in this case, these employees took it to the extreme, and actually falsified the sale of products and services in order to earn more compensation.

Fortunately, in the world of financial advisory services and wealth management, there is a trend occurring which may serve to help restore the public trust. There is a new awareness of the need for financial advisors and service providers to act as trusted fiduciaries for their clients, which may begin to reverse this crisis in public trust.

Financial Advisors as Fiduciaries

If you search the word “Fiduciary” on Wikipedia, you will find the following definition:

A fiduciary is a person who holds a legal or ethical relationship of trust with one or more other parties. In a fiduciary relationship, one person, in a position of vulnerability, justifiably vests confidence, good faith, reliance, and trust in another whose aid, advice or protection is sought in some matter. In such a relation good conscience requires the fiduciary to act at all times for the sole benefit and interest of the one who trusts.

This is a perfect definition of the ideal relationship between a financial advisor and his or her client, which should ideally hinge on the client’s implicit trust that the advisor will at all times act solely in the best interest of the client.

Most financial advisors are fiercely client-centric in their advice and their fees, and behave like fiduciaries for their clients. However, the financial services industry, and its various regulatory bodies, have employed a vague set of suitability guidelines and compensation schemes which have muddied the waters for many consumers, and have left room for potential conflicts of interest. It is not always clear to consumers that their advisor is acting as their fiduciary, and in particular that their advisor’s financial interests are aligned with their own.

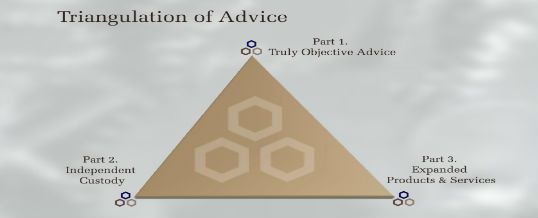

Fortunately for consumers, the financial services landscape is changing rapidly and in dramatic ways. In particular, there is a trend in place we call “The Triangulation of Advice” which is creating alignment with client interests.

The Triangulation of Advice

In recent years, as the financial services industry has consolidated, several very large financial services companies have emerged, based on a service model which delivers several services from a single “Silo”: The combination of financial advice, custody and safekeeping of your assets, and delivery of products and services all delivered under one roof.

This model has worked quite well, as it has allowed big firms to create efficiency, scale, and profitability, while also offering consumers the promise of convenience. Big firms have the size and scale to do all 3 jobs quite well, and consumers can achieve the convenience of “one stop shopping”, when your advisor works for the same firm which acts as custodian of your money, and produces many of the products and services you utilize.

However, the downside of this “single silo” model is that compensation arrangements can become less than clear, and conflicts of interest can result. In particular, when products and services are bundled with the delivery of advice, you may be uncertain how much in fees the firm is charging on the custody, products and services you use – and how much of that compensation is flowing to your financial advisor. As a result, you may be left unsure of whether your advisor is advocating the use of certain products and services because it is best for you, or because he and/or his firm makes more money that way.

Recently there has been significant growth in the population of advisors who are joining a trend we call “The Triangulation of Advice” and moving from being captive employees, to becoming independent advisors with no affiliation to any custodian, or product and service provider. In so doing, many advisors can now provide advice separate from where products are sourced and client assets are held in custody, and clients can access each function separately:

- Advice. As potential conflicts of interest are removed, clients can feel more confident in receiving advice that is transparent, objective, and conflict free, from an advisor who is acting as your agent and fiduciary in selecting the most appropriate products and services, without any affiliation with any single financial institution.

- Custody. Decisions about where to hold your investment assets in custody can be made independently and objectively, as opposed to being forced to hold custody at your advisor’s firm. This can reinforce the safety of your assets from fraud or other risks – by employing a solid third party for the safekeeping of your assets, you can rely on that institution to do only one job, which is to protect your assets from fraud, and accurately report your assets to you on a monthly basis. Because this custodian has no affiliation with your advisor, their job is even to protect your assets from potential acts of fraud by him or her!

- Products and Services. In this new model, and thanks to the advent of technology, clients and their advisors can now become “a client of Wall Street”. An independent fiduciary advisor is now in a position to seek the very best from every firm on Wall Street – from trading, to investment products, lending services, life insurance, etc – on your behalf.

By “Triangulating” these 3 critical areas of service delivery, many advisors are now in a position to act as a true fiduciary for you and your family, and to maximize the level of transparency, objectivity, and freedom from conflicts of interest which you require.

Leave A Comment